MTD Quarterly Updates: What to Report and When

MTD quarterly updates require you to report your total income and expenses by category to HMRC four times a year. You are NOT sending individual transactions — just category totals. The deadlines are 7 August, 7 November, 7 February, and 7 May.

Updates per year

4 quarterly + 1 Final Declaration

What you submit

Category totals, not individual transactions

Q1 deadline

7 August

Q2 deadline

7 November

Q3 deadline

7 February

Q4 deadline

7 May

Final Declaration

31 January following year end

Default accounting method

Cash basis (sole traders from Apr 2024)

Compliant without the manual work

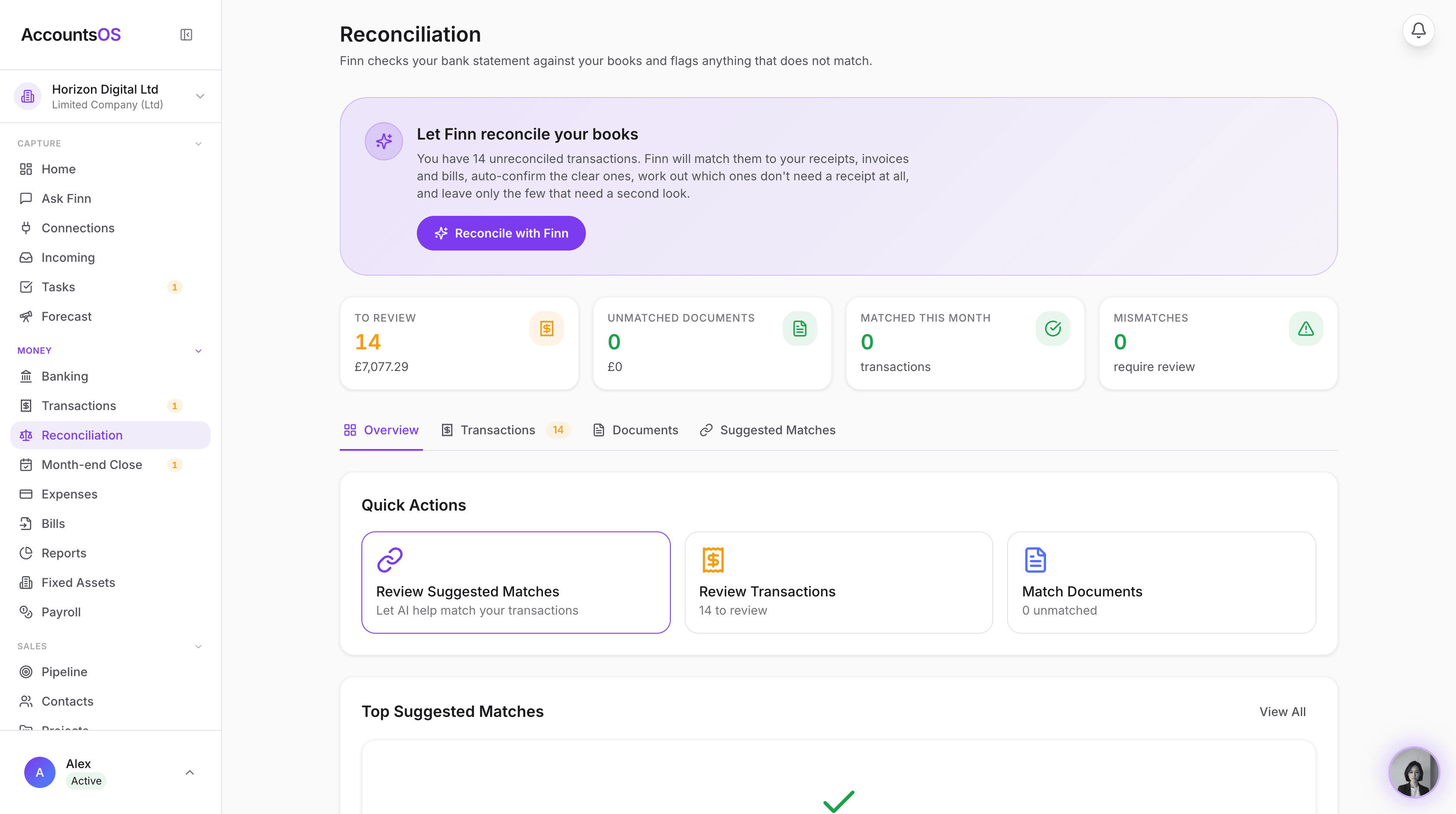

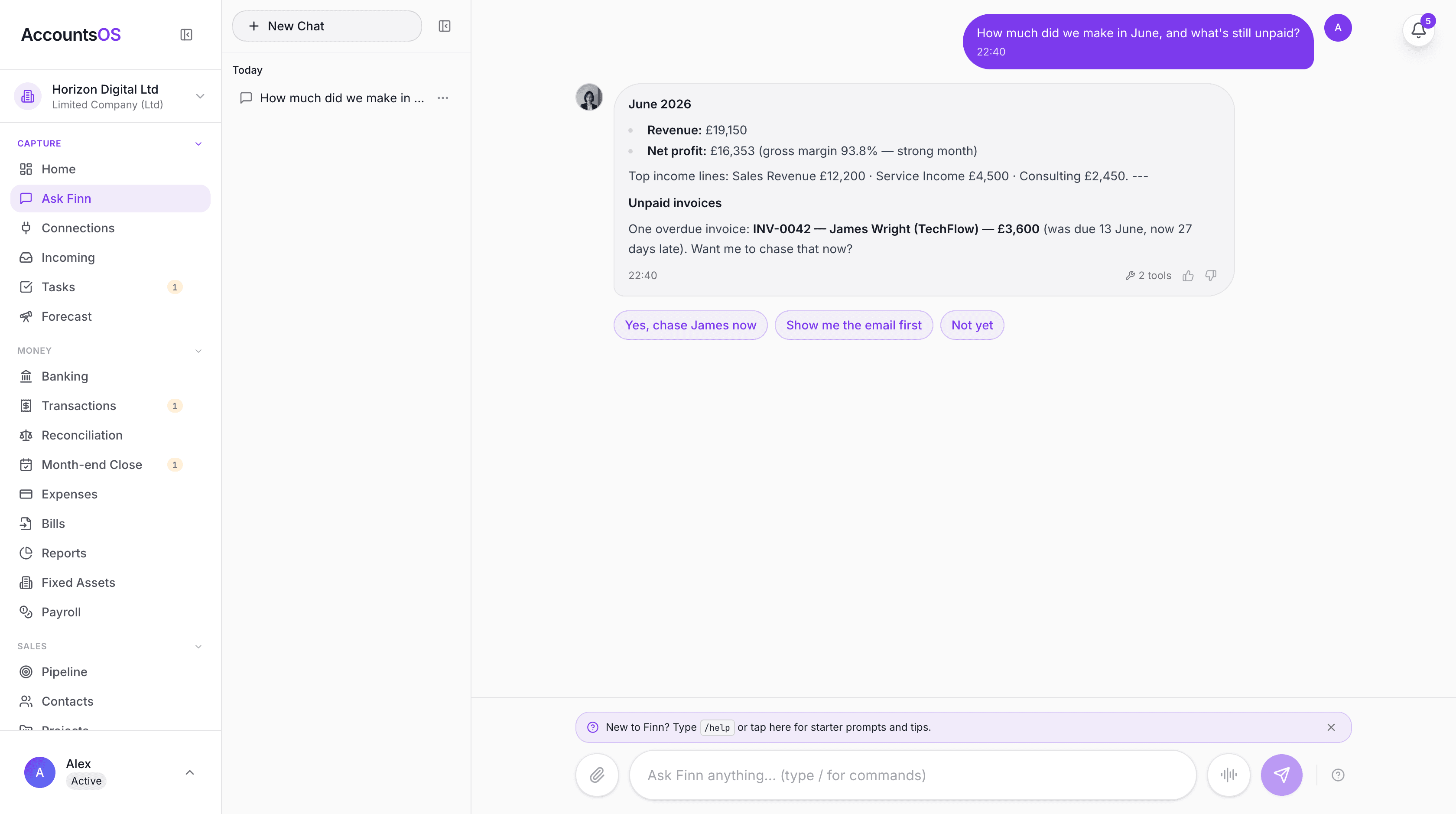

Making Tax Digital means keeping digital records and filing through software. AccountsOS does both for you. Connect your bank and HMRC, and Finn keeps the records, builds the return from your bookkeeping, and files it on your confirmation.

- Digital records kept automatically as money moves

- Returns calculated from your ledger, no bridging spreadsheet

- Submit directly to HMRC once you've checked the figures

- Every deadline tracked so nothing is filed late

Quarterly updates are the core obligation of Making Tax Digital for Income Tax. Four times a year, you must report your income and expenses to HMRC through MTD-compatible software. This is not a mini tax return — it is a progress report on your business finances. Many people are nervous about quarterly updates because they assume it means four times the work. In reality, if your records are kept digitally throughout the quarter, submitting is a matter of confirming the figures and pressing submit. This guide explains exactly what information HMRC requires, the categories you need to report against, and how quarterly updates differ from your annual Final Declaration.

What a Quarterly Update Actually Is

A quarterly update is a summary of your business income and expenses for a three-month period, submitted to HMRC through MTD-compatible software. Critically, you are not sending individual transactions. You are sending category totals. If you had 47 expense transactions for travel during Q1, HMRC receives one figure: total travel expenses for Q1. Your software calculates these totals from your records and submits them. The update is not a tax calculation. HMRC is not working out your tax liability from quarterly updates. The purpose is to give HMRC a running picture of your income and expenses throughout the year, and to give you a better understanding of your tax position as the year progresses. You do not need to pay any tax with your quarterly update. Payment dates for Self Assessment remain unchanged (31 January and 31 July). Quarterly updates are reporting obligations only. Think of it like weighing yourself weekly rather than once a year. The weigh-in does not change anything — it just gives you more frequent data to work with.

What Information to Include

Each quarterly update includes two main components: **1. Income** — The total income received (or invoiced, depending on your accounting method) during the quarter, broken down by HMRC's income categories. **2. Expenses** — The total expenses incurred during the quarter, broken down by HMRC's expense categories. Your MTD software will present these categories for you and calculate the totals from your recorded transactions. You confirm the figures are correct and submit. If you have both self-employment income and property income, you submit separate summaries for each income source. A self-employed plumber who also rents out a flat would submit two sets of figures in each quarterly update. You do not need to include: - Individual transaction details - Copies of receipts or invoices - Bank statements - Capital expenditure (this goes in the Final Declaration) - Personal expenses However, you must keep the underlying records (receipts, invoices, bank statements) digitally for at least 5 years and 10 months after the tax year end, in case HMRC queries your figures.

HMRC Income Categories for Self-Employment

For self-employment income, HMRC requires you to report under these categories: - **Turnover** — Your total business income from sales of goods or services - **Other business income** — Any other income related to the business (e.g., commission, tips, grants) Most sole traders will only use the Turnover category. The split between turnover and other income matters for certain tax calculations, so categorise accurately. If you use the cash basis of accounting, report income when you receive payment. If you use the traditional accruals basis, report income when you invoice (regardless of when you are paid).

| Category | What to Include | Example |

|---|---|---|

| Turnover | Sales of goods or services | Consulting fees, product sales, freelance work |

| Other business income | Non-trading business income | Bank interest on business account, grants, commission |

HMRC Expense Categories for Self-Employment (Trades)

HMRC requires self-employment expenses to be categorised under these standard headings. Your MTD software will use these categories:

| Category | What to Include | Examples |

|---|---|---|

| Cost of goods sold | Direct costs of goods you sell | Raw materials, stock purchased for resale, packaging |

| Construction costs | CIS-related construction expenses | Subcontractor payments (CIS scheme) |

| Travel costs | Business travel (not commuting) | Train tickets, fuel for business trips, flights, parking |

| Car, van and travel expenses | Vehicle costs for business use | Mileage at HMRC rates, vehicle insurance, MOT, repairs |

| Wages, salaries and staff costs | Employee-related costs | Salaries, employer NI, pensions, temp staff |

| Rent, rates and power | Premises costs | Office rent, business rates, electricity, gas, water |

| Repairs and maintenance | Repairs to business assets | Equipment repairs, premises maintenance, tool replacement |

| Accountancy, legal and professional fees | Professional services | Accountant fees, solicitor fees, professional memberships |

| Interest and bank charges | Financial costs | Loan interest, bank charges, overdraft fees |

| Phone, fax, stationery and other office costs | General admin | Phone bills, internet, postage, stationery, software subscriptions |

| Advertising and marketing | Promotion costs | Website, ads, business cards, trade show fees |

| Business insurance | Insurance premiums | Professional indemnity, public liability, employer's liability |

| Other business expenses | Anything not covered above | Training, subscriptions, tools under £1,000 |

HMRC Expense Categories for Property Income

If you have UK property income, HMRC uses different categories:

| Category | What to Include | Examples |

|---|---|---|

| Rent received | Total rental income | Monthly rent from tenants, holiday let income |

| Rent, rates and insurance | Property running costs | Ground rent, council tax (if you pay it), buildings insurance |

| Property repairs and maintenance | Repair costs | Plumber, electrician, decorating, appliance repairs |

| Loan interest and financial costs | Mortgage and finance | Mortgage interest (subject to restriction), arrangement fees |

| Legal, management and professional fees | Professional costs | Letting agent fees, solicitor fees, accountant fees |

| Cost of services provided | Tenant services | Cleaning, gardening, communal area maintenance |

| Other property expenses | Anything else | Travel to property, advertising for tenants, safety certificates |

The Four Quarterly Deadlines

The MTD tax year is divided into four quarters that align with the standard UK tax year (6 April to 5 April):

| Quarter | Period Start | Period End | Submission Deadline | Days to Submit |

|---|---|---|---|---|

| Q1 | 6 April | 5 July | 7 August | 33 days |

| Q2 | 6 July | 5 October | 7 November | 33 days |

| Q3 | 6 October | 5 January | 7 February | 33 days |

| Q4 | 6 January | 5 April | 7 May | 32 days |

Cash Basis vs Traditional Accounting

How you record income and expenses in your quarterly updates depends on which accounting method you use. **Cash basis** (most common for sole traders): - Record income when you receive payment - Record expenses when you pay them - Simpler to manage — matches your bank statements - Available if your gross income is under £150,000 - Default method for sole traders since April 2024 **Traditional accruals basis**: - Record income when you invoice (even if not yet paid) - Record expenses when you incur them (even if not yet paid) - More complex — requires tracking debtors and creditors - Required for partnerships and those over £150,000 income - Gives a more accurate picture of business performance For most sole traders and landlords, the cash basis is the right choice. It is simpler, matches what you see in your bank account, and is now the default. You only need to opt for the accruals basis if you have specific reasons (e.g., you want to claim relief on bad debts, or you have significant work in progress). Your MTD software will handle the accounting method for you — just make sure you tell it which method you are using when you set up.

| Feature | Cash Basis | Accruals Basis |

|---|---|---|

| Income recorded | When received | When invoiced |

| Expenses recorded | When paid | When incurred |

| Complexity | Lower | Higher |

| Income limit | £150,000 gross | No limit |

| Default for sole traders | Yes (from April 2024) | No — must opt in |

| Bad debt relief | Not available | Available |

What If Your Quarterly Figures Are Wrong?

Quarterly updates are not final. If you realise that your Q1 figures were incorrect — perhaps you missed an expense or double-counted some income — you can correct this in subsequent quarterly updates or in your Final Declaration. HMRC expects reasonable accuracy in quarterly updates but recognises that they are in-year estimates based on available information. You are not expected to have finalised accounts at the quarterly stage. Specifically: - **Minor corrections**: Adjust in the next quarterly update. If you forgot a £50 expense in Q1, include it in Q2. - **Significant corrections**: Your MTD software should allow you to amend a previously submitted quarterly update. If a large invoice was categorised incorrectly, amend the relevant quarter. - **Year-end adjustments**: The Final Declaration is where you finalise everything. Capital allowances, pension contributions, loss relief, and other annual adjustments go here. The key principle: quarterly updates get your figures roughly right throughout the year. The Final Declaration makes them exactly right. Do not stress about perfection in quarterly submissions — accuracy is more important than precision at this stage.

The Final Declaration: How It Differs from Quarterly Updates

After your four quarterly updates, you must submit a Final Declaration by 31 January following the end of the tax year. This replaces the traditional Self Assessment tax return. The Final Declaration is where you: - **Confirm or adjust** your quarterly figures for the full year - **Add income from other sources** — employment, dividends, savings interest, pensions - **Claim capital allowances** — for equipment, vehicles, and other capital expenditure - **Claim tax reliefs** — pension contributions, charitable donations, loss relief - **Declare other information** — student loan repayments, High Income Child Benefit Charge, etc. - **Calculate your final tax liability** for the year The Final Declaration is more comprehensive than quarterly updates. While quarterly updates cover business income and expenses only, the Final Declaration covers your complete tax position for the year. For the 2026/27 tax year, your Final Declaration is due by 31 January 2028. This deadline carries full Self Assessment penalties — unlike quarterly updates in the soft landing year, there is no leniency on the Final Declaration deadline. Your MTD software will guide you through the Final Declaration process, pulling in your quarterly data and prompting you for additional information needed to complete the return.

| Feature | Quarterly Update | Final Declaration |

|---|---|---|

| Frequency | 4 times per year | Once per year |

| Content | Business income + expenses by category | Complete tax position |

| Deadline | 7 Aug, 7 Nov, 7 Feb, 7 May | 31 January |

| Capital allowances | Not included | Included |

| Other income sources | Not included | Included |

| Tax calculation | Estimate only | Final liability |

| Soft landing (2026/27) | No penalty points | Full penalties apply |

| Payment due | No | Yes (balancing payment) |

Frequently asked questions

Do I have to submit every individual transaction to HMRC?

No. Quarterly updates contain category totals only. If you had 100 transactions in Q1, HMRC receives summary figures by category — not the 100 individual transactions. Your software calculates the totals from your records.

Do I have to pay tax with each quarterly update?

No. Quarterly updates are reporting obligations only. Payment dates for Self Assessment remain unchanged — you pay on 31 January and 31 July as before. No new payment dates are created by MTD.

What if I have no income or expenses in a quarter?

You should still submit a quarterly update showing zero figures. A nil return is still a return, and failing to submit one could result in a penalty point (from 2027/28 onwards). Most MTD software makes nil returns very quick.

Can I correct mistakes in a quarterly update?

Yes. You can amend a previously submitted quarterly update through your MTD software, or make corrections in the next quarter's update. The Final Declaration is where everything is finalised, so minor quarterly errors are not a serious concern.

What accounting categories does HMRC use for expenses?

HMRC uses standard categories including cost of goods sold, travel costs, wages, rent/rates/power, repairs, professional fees, interest, office costs, advertising, insurance, and other expenses. Your MTD software will map your transactions to these categories.

Should I use cash basis or accruals for quarterly updates?

Most sole traders should use the cash basis, which is now the default. It records income when received and expenses when paid, matching your bank statements. Use accruals only if you need bad debt relief, have significant work in progress, or your income exceeds £150,000.

How long do quarterly updates take to complete?

If your records are kept up to date digitally throughout the quarter, submitting should take 10-15 minutes — reviewing the category totals and pressing submit. The time-consuming part is keeping records throughout the quarter, not the submission itself.

What is the difference between a quarterly update and the Final Declaration?

Quarterly updates cover business income and expenses only. The Final Declaration is a complete tax return covering all income sources, capital allowances, reliefs, and your final tax calculation. Quarterly updates are progress reports; the Final Declaration is the definitive annual return.

Do I need to include personal expenses in quarterly updates?

No. Only business income and business expenses are included in quarterly updates. Personal expenses, even if paid from a business account, should be excluded. If you use your business account for personal spending, categorise those transactions as drawings/personal.

What happens if I submit a quarterly update late during the soft landing year?

During the 2026/27 soft landing year, no penalty points are issued for late quarterly updates. HMRC will still record that the submission was late and may send reminders, but there is no financial consequence. The Final Declaration deadline of 31 January 2028 is still enforced.

Related MTD guides

Making Tax Digital Penalties: Late Submission Fines Explained

MTD uses a points-based penalty system. Each late submission earns 1 penalty point. When you reach 4 points, you receive a £200 fine. The good news: the soft landing year (2026/27) means no penalty points for late quarterly updates — but the Final Declaration deadline of 31 January 2028 is still enforced.

Making Tax Digital April 2026: Your Action Plan

Making Tax Digital for Income Tax starts 6 April 2026 for anyone with qualifying income (self-employment + UK property, gross, combined) over £50,000. If this applies to you, you must sign up for MTD, choose compatible software, and start keeping digital records from 6 April 2026.

Best MTD Software UK 2026: Free and Paid Options Compared

Several free MTD-compatible software options exist for UK taxpayers, including QuickFile, My Tax Digital, and FreeAgent (free via NatWest or Mettle banking). Paid all-in-one options include Xero, QuickBooks, and Sage. AccountsOS is MTD-compatible software that uses AI to do the bookkeeping for you and submits your VAT return directly to HMRC, from £20 a month after a 14-day free trial.

How to Sign Up for Making Tax Digital for Income Tax

You must sign up for Making Tax Digital for Income Tax through the HMRC online service before 6 April 2026 if your qualifying income exceeds £50,000. You'll need your Government Gateway ID, UTR, NI number, and to have chosen MTD-compatible software before signing up.

Get MTD-ready with AccountsOS

Connect your bank and HMRC, and let Finn keep the records, build the return and submit it for you. Be ready for Making Tax Digital without the admin.

Free for 14 days. No credit card required.